Truck insurance in the United States continues to evolve alongside rising vehicle costs, shifting driver behavior, and changing risk patterns. Unlike traditional auto insurance, truck insurance reflects a broader set of risks, including heavier vehicles, higher repair costs, and increased liability exposure.

Understanding current truck insurance statistics is essential for anyone researching costs, coverage trends, or market dynamics. At QuoteFlow Marketing we’ve gathered and wrote a data-driven breakdown of the most important figures shaping the U.S. truck insurance landscape.

Average Truck Insurance Statistics

Truck insurance costs vary widely depending on truck type, usage, and driver profile. However, several key benchmarks help define the market:

- The average annual cost of truck insurance ranges from $1,100 to $3,000 for personal-use trucks.

- Full-coverage truck insurance typically averages $150 to $240 per month.

- The national average auto insurance cost (including trucks) reached approximately $2,500+ annually in recent years, reflecting broader insurance inflation

- Truck insurance premiums have increased significantly over the past decade due to higher claim costs and repair inflation.

- Owner-operators running commercial trucks under their own authority pay an average of $900–$1,800 per month for insurance, while leased operators typically pay $250–$500 per month.

This pricing gap reflects the higher risk and coverage requirements independent operators carry, and why they consistently generate some of the most active demand in the market. For agencies looking to tap into that demand, commercial truck insurance leads play a critical role in reaching owner-operators who are actively comparing coverage and pricing.

As per the latest truck insurance statistics, pickup trucks often cost more to insure than smaller vehicles because of their size, repair costs, and accident impact severity.

Average Truck Insurance Costs by Use Type

Truck insurance costs vary significantly based on how the vehicle is used. The biggest distinction is whether the truck is used for personal purposes or as part of a commercial operation. These truck insurance statistics show that insurers assess risk very differently in each case, which is why pricing can range from a few thousand dollars to well over $20,000 annually.

Personal-Use Trucks

Average: $1,500 to $2,800 per year

Trucks used strictly for personal driving, such as commuting, errands, or occasional hauling, are the least expensive to insure. These policies are similar to standard auto insurance but may carry slightly higher premiums due to the size and value of trucks.

Rates in this category are influenced by:

- Driver history and age

- Location and driving frequency

- Truck make, model, and value

- Coverage limits and deductibles

Because there is no business exposure, insurers consider personal-use trucks relatively low risk compared to commercial vehicles.

Commercial Trucks (Owner-Operators with Authority)

Average: $9,000 to $17,000 per year

Owner-operators with their own authority face significantly higher insurance costs because they operate as independent businesses. These policies must include multiple coverage types, such as primary liability, cargo insurance, and physical damage.

Premiums vary based on:

- Operating radius (local vs. long-haul)

- Type of freight (general goods vs. hazardous materials)

- Claims history and driving record

- DOT compliance and safety scores

Since these drivers are fully responsible for their operations, according per the recent truck insurance statistics insurers price in a higher level of risk exposure.

Leased Operators (Under Another Carrier’s Authority)

Average: $3,000 to $5,000 per year

Leased owner-operators generally pay much less for insurance because they operate under a motor carrier’s authority. The primary liability coverage is often provided by the carrier, leaving the driver responsible for limited coverage such as bobtail or non-trucking liability.

Costs depend on:

- Lease agreement terms

- Required supplemental coverage

- Driving history

- Equipment value

This setup reduces the individual driver’s insurance burden, making it a more affordable entry point into the trucking industry.

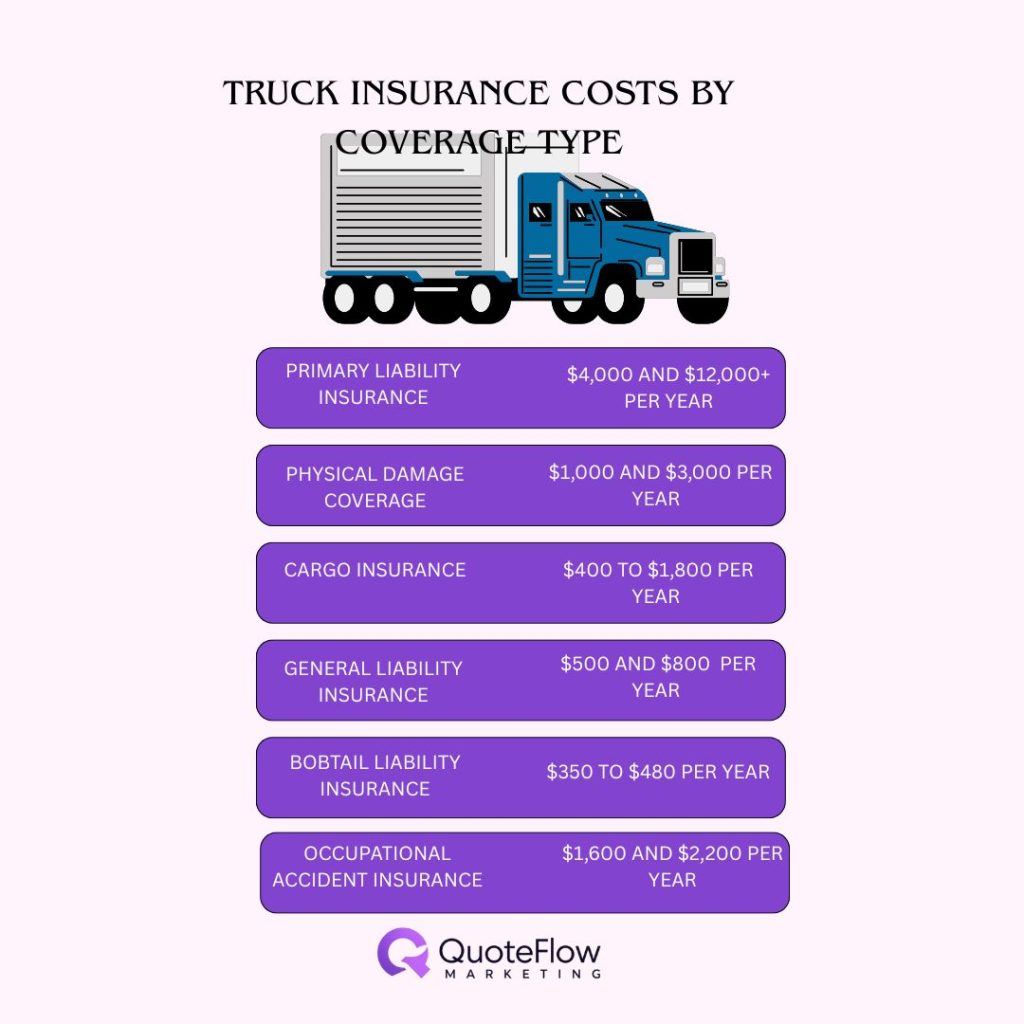

Truck Insurance Costs by Coverage Type

When people look at truck insurance pricing, they often focus on the total number. But what really matters is how that number is built. A truck insurance policy isn’t one single cost, it’s a combination of different coverages, each priced based on a specific type of risk.

Some of these coverages are mandatory, others are optional, but together they determine how protected your operation actually is.

Primary Liability Insurance

The biggest piece of the puzzle is primary liability insurance, which typically runs between $4,000 and $12,000+ per year. This is the coverage that pays for injuries or property damage you cause to others on the road. Because it’s required and tied directly to risk exposure, like how far you drive, what you haul, and your driving history, it usually makes up the largest share of your premium.

Physical Damage Coverage & Cargo Insurance

Next is physical damage coverage, which generally costs between $1,000 and $3,000 annually. Instead of protecting others, this one protects your truck itself. Whether it’s a collision, theft, or storm damage, this is what covers repair or replacement. The newer and more expensive your truck is, the more you’ll pay here.

Then there’s cargo insurance, typically ranging from $400 to $1,800 per year. This covers the freight you’re hauling. The cost can stay relatively low for general goods, but it climbs quickly if you’re transporting high-value or theft-prone items. In many cases, brokers won’t even work with you unless you carry this coverage.

General Liability Insurance & Bobtail Liability Insurance

Another piece that often gets overlooked is general liability insurance, which usually falls between $500 and $800 annually as shown in the latest truck insurance statistics. This has nothing to do with driving—it covers everyday business risks, like someone getting injured at your office or damage happening during loading and unloading. It’s not always required, but it adds an extra layer of protection beyond the road.

If you’re leased onto a carrier, you’ll likely also need bobtail or non-trucking liability insurance, which costs around $350 to $480 per year. This fills the gap when you’re driving without a load or outside of dispatch, situations that aren’t covered under a motor carrier’s primary policy.

Occupational Accident Insurance

For driver protection, many owner-operators choose occupational accident insurance, which typically runs between $1,600 and $2,200 per year. This helps cover medical bills and lost income if you’re injured on the job. It’s especially common for independent contractors who don’t carry traditional workers’ compensation.

Liability Limits and Insurance Requirements

Liability coverage is at the core of every truck insurance policy, and it’s one of the biggest factors behind the final price.

At the federal level, the minimum requirement set by the Federal Motor Carrier Safety Administration (FMCSA) is $750,000. But in reality, most truckers don’t operate at that level for long. If you’re hauling hazardous materials, the requirement can jump as high as $5 million, and even for standard freight, the industry expectation is usually at least $1 million in coverage.

The reason is simple: brokers and shippers often won’t work with carriers who only carry the minimum. Higher limits make you easier to work with and open the door to better loads.

Of course, increasing your liability limit will raise your premium, but it also protects you from large claims and makes your business more competitive. For most operators, it’s less of a cost decision and more of a business necessity.

U.S. Truck Insurance Market Trends

All of these truck insurance statistics show that truck insurance isn’t just getting more expensive, —it’s also becoming more sophisticated.

The latest truck insurance statistics, show the global truck insurance market growing from about $166.99 billion in 2026 to over $341 billion by 2035. A big reason behind that growth is how insurers are pricing risk today.

Liability coverage alone makes up roughly 70% of most policies, reinforcing how central it is to overall costs. At the same time, nearly half of policies now use telematics—real driving data—to determine pricing, rather than relying only on traditional factors.

Another telling stat: more than 90% of interstate carriers in the U.S. carry higher-than-minimum liability limits. That’s a clear sign that the market has moved beyond basic compliance and toward risk management.

Overall, the trend is shifting toward data-driven pricing, where how you actually operate matters more than just who you are on paper.

Conclusion

Truck insurance costs in the U.S. continue to move in one clear direction, upward, but with more precision behind how those costs are calculated.

As these truck insurance statistics show, pricing is no longer based only on basic factors like age or location. Instead, insurers are looking deeper at how trucks are used, what risks they carry, and how drivers actually operate on the road.

Sources:

https://www.plummerinsurance.com/how-much-does-truck-insurance-cost/

https://www.insure.com/car-insurance/most-least-expensive-pick-ups-insure.html

https://northpennnow.com/news/2026/apr/07/how-much-is-semi-truck-and-trailer-insurance-in-the-us

https://www.atob.com/blog/owner-operator-truck-insurance-cost-statistics

https://vaticinsurance.com/commercial-truck-insurance-guide/

https://www.caranddriver.com/car-insurance/a36320549/truck-insurance-cost

https://www.selectinsgrp.com/cargo-insurance-for-truckers

https://schneiderowneroperators.com/owner-operator-tips/how-much-semi-truck-insurance

https://truckaccidents.com/blog/truck-insurance-minimum-overview/

https://www.businessresearchinsights.com/market-reports/commercial-truck-insurance-market-102830